Today’s business leaders face stresses from all directions – economic challenges (recession or no recession), hiring struggles, supply chain disruptions, inflationary pressures, political turbulence, entitled employee attitudes, and information overload from noisy media.

As leaders juggle with all of these disparate balls in the air, the ball they often take their eye off of is themselves.

Kevin Lawrence, author of Your Oxygen Mask First, led a workshop for business owners and guests of Executive Forums Silicon Valley in downtown San Jose, to help the leaders be a little selfish for the day – to put YOUR OXYGEN MASK FIRST.

Mr. Lawrence is an award-winning business coach and has a passion for educating leaders on the importance of expanding mental health and mental growth and building leadership resilience.

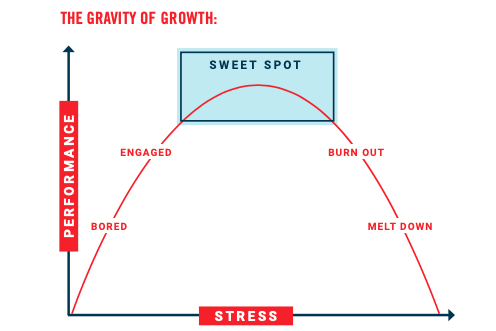

The workshop opened with a discussion of the challenge – driving and maintaining leadership performance at the sweet spot as shown in the graphic below without progressing to burnout and sometimes even meltdown. Mr. Lawrence gave many examples about how leaders experience challenges, and the methodologies for diagnosing issues, as well as resources to use when sliding down the unwanted slope towards meltdown.

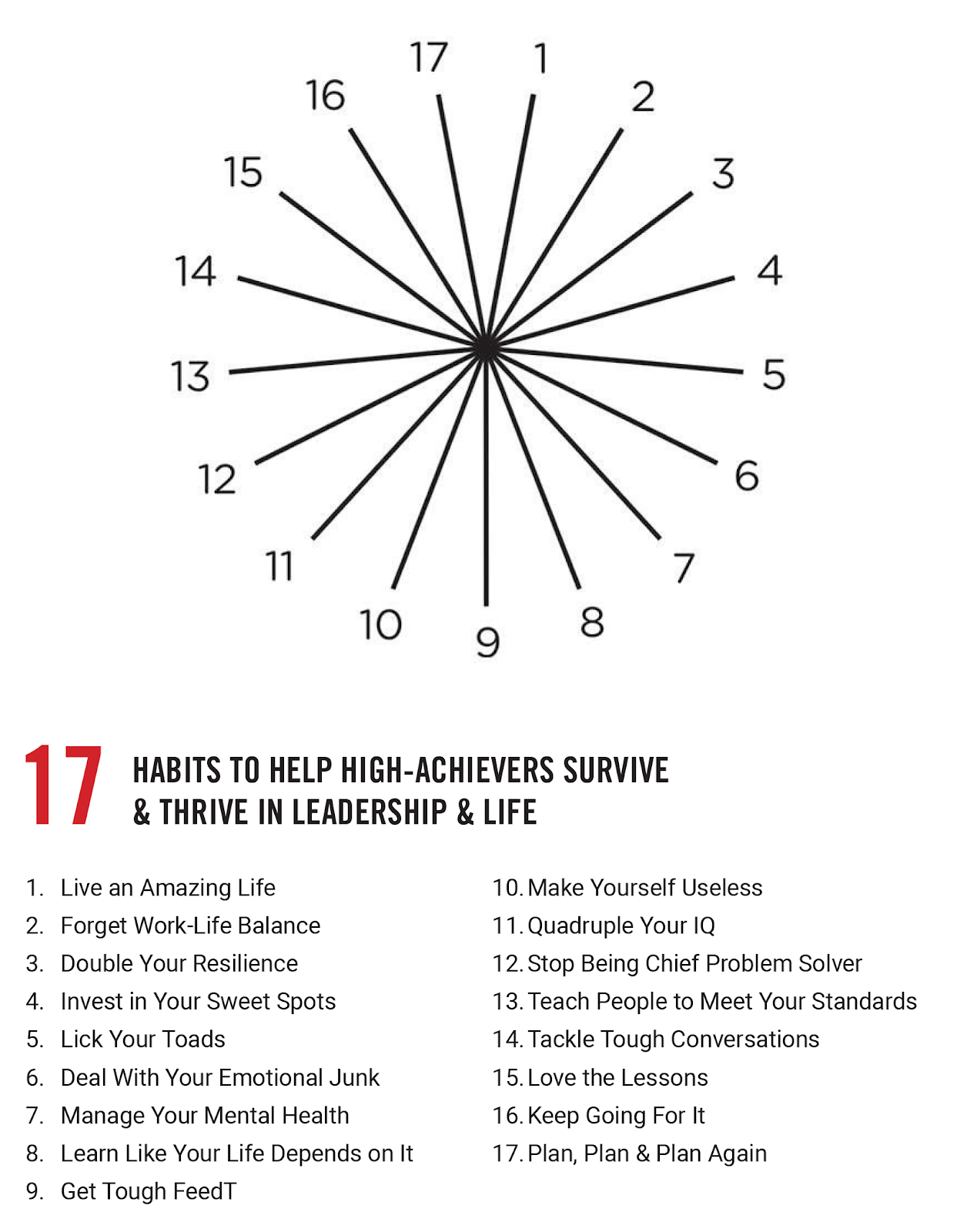

This discussion was followed by a description and a personal assessment of the 17 Habits that help high achievers survive and thrive in both business leadership and life. Each participant created a wheel of satisfaction (polar plot) of how each of the 17 habits below showed up in their life, for identifying key strengths and areas of opportunity.

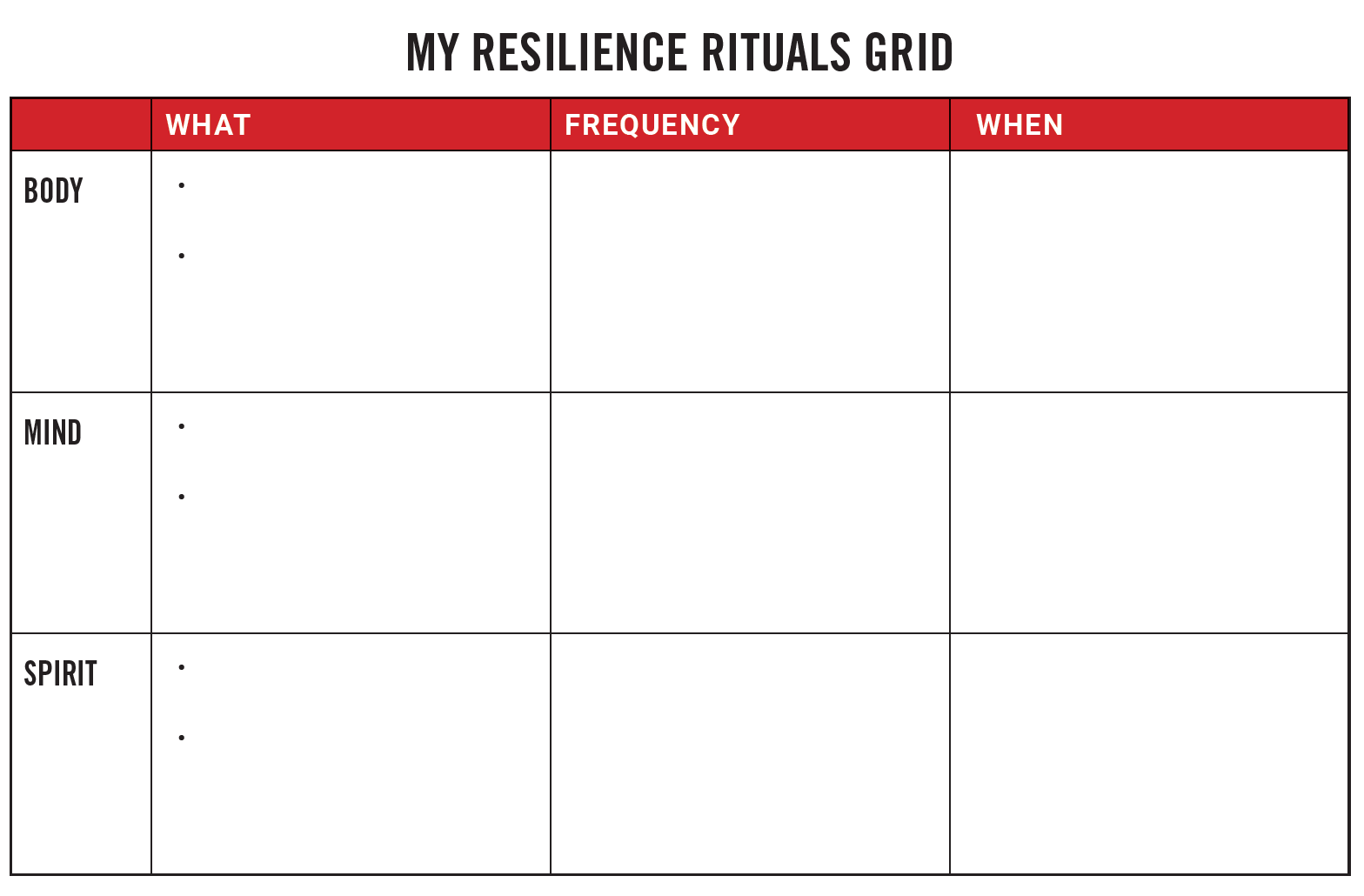

After group discussions around the issue of balance in members’ lives, a set of resiliency habits have created that support a balanced life through specific, timed, and repeated activities to strengthen the body, mind, and soul.

Members and guests shared their existing resiliency habits for making improvements, such as deeply personal rituals specific to each individual leader – from musical instruments, to fitness routines, to bicycling, to meditation, to reading. Feel free to jot down your resiliency rituals using the grid below.

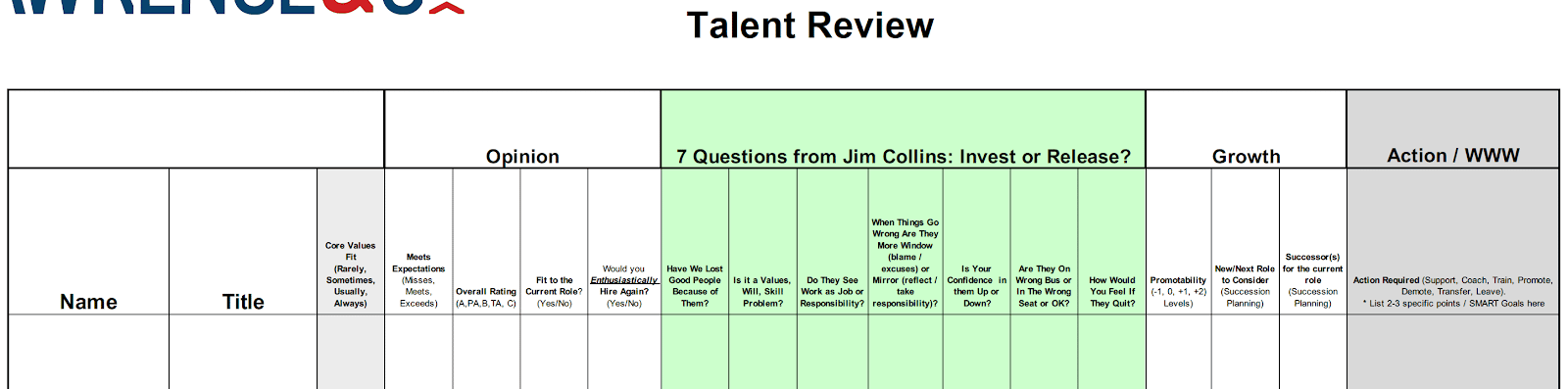

Moving forward from the leader’s resiliency discussion, the group discussed Leadership Habit Number 17 – Make Yourself Useless. This habit revolves around top-grading employees with the objective of building a team that delivers better results than you, or even without you. As stated by Harvey Firestone, “The growth and development of people is the highest calling of leadership”. The group, using a top-grading worksheet, was able to identify and rank employees and establish specific action plans to coach up or coach out.

It was a great session of deep thinking and dynamic exchange that happens monthly at Executive Forums Silicon Valley where we leverage the collective intelligence of the group for the benefit of each individual member.

I want to thank Kevin Lawrence (Lawrence & Co) and recommend that you contact him directly to learn more about his workshops and his book, Your Oxygen Mask First.

A shout out to some Executive Forums Silicon Valley members who celebrated over six years in the Forum – your business leadership and camaraderie are so very much appreciated.

I also want to thank the Silicon Valley Capital Club for the venue, meals, and logistic support. I highly recommend the Club for your events. Please contact Edith Hernandez (edith.hernandez@invitedclub.com) to arrange your next event.

At Executive Forums Silicon Valley, selected business owners and leaders work together to gain clarity, insight, and accountability to ignite their leadership engines, grow their businesses, and improve their lives. If you are interested in learning more about Business Owner Advisory Boards or the Entrepreneurial Operating System (EOS) please contact Glenn Perkins at gperkins@executiveforums.com or call 408-901-0321. For more information visit http://www.execforumssv.com/.

Leaders of 2nd, 3rd, and 4th generation family businesses gathered to learn from each other and enjoy a morning of fun in the awesome SAP Boardroom Suite at Levi’s Stadium, home of the San Francisco 49ers.

The session, hosted by Bridge Bank (Emily Ruvalcaba) and Executive Forums Silicon Valley (Glenn Perkins), was designed around a discussion with panelists Brittni Daley-Grishaeva, Adam Beck, Dee Ann Harn, and Ian Barth who shared lessons learned about the challenges and opportunities in taking over from the previous generations.

Prior to the panel discussion, the attendees participated in a Personal Histories networking activity during breakfast. This was followed by a team scavenger hunt in the 49ers Museum to experience and learn from the culture of a large family business—the San Francisco 49ers.

An intimate panel discussion revolved around themes and questions such as:

How or when did you recognize the “super power” of your predecessor? How were you able to replace that “super power” within the organization? How did you apply your own “super power” within your company

What counsel or guidance would you give to those who are assuming a new leadership position in dealing with or overcoming entrenched personnel in a company?

Looking back, what is the biggest opportunity to shake things up that you identified when transitioning?

Can you comment on what may have been scary for you when you took over your position? What was that particular aspect of the business troublesome for you? What did you do to overcome those fears?

What counsel or guidance about support structures or scaffolding would you give to those who are assuming a new leadership position in a company?

Open questions and discussion based on attendee questions.

It was a fantastic event and we want to thank the attendees and panelists for an awesome morning and for being so open to sharing their experience and expertise with everyone.

If a learning and networking event such as this might be of interest to you and the leaders in your generational business, please reach out.

Leverage Your Time for Bottom Line Results with an Engagement Manager

Investing time in building and maintaining relationships – both external to the organization and internal to the organization – is critical to the success of every CEO.

I recently learned of a structured approach for enhancing relationships by Patrick Ewers, founder and CEO of Mindmaven, a coaching firm that works with leaders AND their assistants.

Using the Mindmaven model — leverage, intent, and fellowship— I began implementing some of these principles within my own business and invited Patrick to share it with members of the Executive Forums Silicon Valley peer groups.

How leaders can “achieve True Greatness by freeing up 8+ hours a week so they can use that time to invest in what truly matters most: relationships.”

Patrick shared with us several hands-on, step-by-step ways in which a CEO can gain leverage to build better relationships by training an executive assistant to become a CEO’s “engagement manager (EM).”

The term Engagement Manager (EM) is not the same as a social media engagement manager, but this role has some of the same results.

An EM is trained by the CEO to address tasks that not only free up a CEO’s time, but can increase relationship building opportunities, thus freeing the CEO to focus on high value activity which impacts bottom line results.

LEVERAGE tactics Patrick suggested:

Voice Communications via Dictation Software

Patrick demonstrated in real time how to leverage an hour or more a day using a phone application to dictate tasks, emails, and meeting notes. Leaders are much better at verbal communication and dictation can be done asynchronously (when time permits as opposed to when the assistant is available). Dictation files are delivered directly to an EM via email, text, or a project management system such as Asana. The EM receives the dictated instructions and moves the requested task forward.

Inbox Shadowing

A second technique discussed was inbox shadowing. By giving an EM access to a CEO’s email for “Inbox Shadowing,” a CEO can trust that emails are sorted by priority so they can move quickly through their inbox. Sorting labels or folders might look like this:

Drafts (responses drafted for CEO review)

Please Handle (emails on which the EM needs CEO input first)

Completed (emails completely handled within authority of the EM)

FYI emails (to read later)

Using dictation and inbox shadowing, an EM can be responsible for drafting follow up emails, meeting debriefs, and pre-meeting planning documents.

Meeting Debriefs and LoopLeverage

With structured and habitualized Meeting Debriefs, a CEO can quickly capture important details from a meeting in a voice dictation sent to their EM who then implements the Mindmaven LoopLeverage technique.

LoopLeverage uses followup tasks, reminders, and tracking in a CRM, calendar, or project management software. These reminders, set for the EM, allow the EM to proactively follow up about promises made to and by the CEO. The personal connection information and business key facts that a CEO learns and shares in their Meeting Debrief dictation also gets tracked by the EM to bring up for robust future meeting conversations.

Together these leverage techniques—Meeting Debriefs and LoopLeverage—help a CEO build trust and stronger relationships while also lifting their mental load, ultimately resulting in increased intent and fellowship, goals of the Mindmaven model.

Culmination of Time, Training, and Small Steps Yield Results

Patrick emphasized that it takes three to six months for a CEO to make these steps natural and train an EM. However, small ideas and steps over time lead to cumulative results that can result in free time for a CEO to generate big ideas. And results.

If you are a leader who could use 8 to 10 hours a week to of free time build business relationships (internal and external) and reduce stress associated with low impact high urgency tasks, I recommend reaching out to Patrick Ewers and the Mindmaven team (www.mindmaven.com/contact) to have a discussion.

At Executive Forums Silicon Valley, selected business owners and leaders work together to gain clarity, insight and accountability to ignite their leadership engines, grow their businesses and improve their lives. If you are interested in learning more about Business Owner Advisory Boards, Entrepreneurial Operating System (EOS), Stages of Growth, Value Builder System or becoming a member at Executive Forum Silicon Valley, please contact Glenn Perkins: gperkins@executiveforums.com or call 408-901-0321. For more information visit http://www.execforumssv.com/.

Executive coach, speaker and author Vitale Buford presented at the Silicon Valley Executive Forum about overcoming perfectionism in May 2021.

She started by quoting Brene Brown: “Perfection is a 20-ton shield that we lug around thinking it will protect us when, in fact, it’s the thing that’s really preventing us from taking flight.”

Striving for excellence is a positive passion and a self-initiated drive that makes a great CEO or a leader, while being a perfectionist is allowing one’s worst critique constantly judging oneself as a bystander. A perfectionist mindset is based on limiting beliefs about oneself and others, and is mentally, emotionally and psychologically debilitating.

Symptoms of perfectionism in work and in life

Symptoms of perfectionism can be:

People-pleasing

Approval seeking

Control

Avoiding conflict

Anxiety and fear

Obsessive thoughts

High expectations

Low self-worth

Comparison

Procrastination

Feeling stuck

Indecision

Perfectionism is manifested in our careers like this:

In identifying patterns of perfectionist behaviors, Ms. Buford listed “slow and fast perfectionism” for our intentional observation:

Slow:

Procrastination

Indecision

Fear of failure

Imposter Syndrome

Feeling stuck

Anxiety

Black and white thinking

Avoiding conflict

Fast:

Approval seeking

People pleasing

Unrealistic expectations for yourself and others

Obsessive thinking

Need for control

“Work harder, achieve more” thinking

Constant overwhelm

Both slow and fast perfectionism can negatively affect our relationships, personal development, family and parenting, finances, health, fun and enjoyment and the ability to lead oneself and others.

Step 2: Mindset Change

Ms. Buford suggested using “habit of self-compassion”, summarized as “Four Cs” - criticism, curiosity, compassion, and choice, - to reframe perfectionist way of thinking, with mantras and routines:

Notice your Criticism

Get Curious

Show yourself Compassion

Choose better

Step 3: Action

What does it take to build habits of self-compassion, other than time?

“Reframing, mantras, routines” are the three words Ms. Buford used to conclude her presentation.

To get out of the negative and self-destructive habits of thinking, first refrain from thinking “what if…”, insead, think “even if…”. Refrain from viewing anxiety-causing unknown as “uncertainty”, but to view it as “possibility”. Refrain from constantly doing the “balancing” acts of pleasing everyone, and start to actively pursue your own “priority”.

Mantras like these ones below can also help us feel good about ourselves:

“I give myself room to be human.”

“Done is better than perfect.”

“I cannot miss out on what’s meant for me.”

Action leads to confidence leads to action.

Creating new routines to reinforce new habits of thinking can gradually lead to changing perfectionist behaviors.

To get more information about overcoming perfectionism, please contact @VitaleBuford

At Executive Forums Silicon Valley, selected business owners and leaders work together to gain clarity, insight and accountability to ignite their leadership engines, grow their businesses and improve their lives. If you are interested in learning more about Business Owner Advisory Boards, Entrepreneurial Operating System (EOS), Stages of Growth, Value Builder System or becoming a member at Executive Forum Silicon Valley, please email Glenn Perkins: gperkins@executiveforums.com or call 408-901-0321. For more information visit http://www.execforumssv.com/.

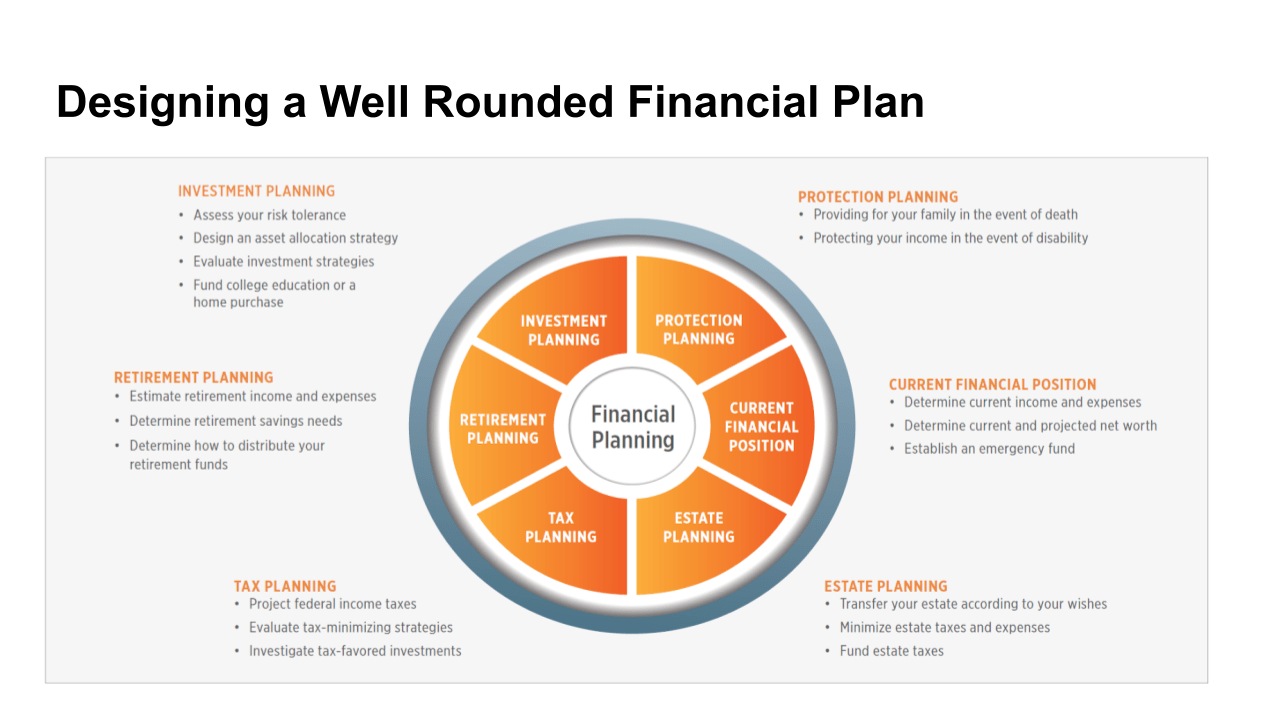

Financial planner and wealth advisor Stephen Grochol of SGC Financial Services presented at the Executive Forum Silicon Valley in 2021 about all major six areas of financial planning: Current financial position, retirement planning, insurance protection planning, investment planning, estate planning and tax planning.

To put all pieces together AND to accomplish one’s retirement goals, these steps need to be taken:

“You don’t know where you are going if you don’t know where you are…” said Mr. Grochol. Whether an individual or a couple, the first place to start is a current year’s balance sheet that breaks down assets and liabilities, as well as percentage for asset types such as cash, taxable investments, qualified retirement, life insurance and real estate. This first step is to:

Determine current income and expenses

Determine current and projected net worth

Establish an emergency fund

Retirement planning

To prepare for retirement, you need to

Estimate retirement income and expenses

Determine retirement savings needs

Determine how to distribute your retirement funds

To determine if an individual or a couple have enough funds for retirement, projections will be made for possible retirement preferences such as

For most of the aging retirees, long term care costs can be significant without adequate long term care insurance. In the event of disability, not only will there be substantial draining of wealth, but there is also the opportunity cost as the lost investment growth on the money used for paying for care from income or from existing investments. It is important to do the following planning long before retirement:

Longer term care insurance planning

Life insurance effect on protection planning and estate transfer

Long term disability

Health insurance

Liability insurance

Investment planning

One important way of wealth accumulation is through investment, which requires one to

Assess your risk tolerance

Design an asset allocation strategy

Evaluate investment strategies

Fund college education or a home purchase

Asset allocation depends on each person’s risk tolerance. Mr. Grochol presented this question for members of the Executive Forum to determine their own risk tolerance:

Which of the following statements would best describe your reaction if the value of your portfolio were to suddenly decline by 15%?

I would be very concerned because I can’t accept fluctuations in the value of my portfolio.

If the amount of income I receive was unaffected, it wouldn’t bother me.

Although I invest for long-term growth, even a temporary decline would concern me.

Although I invest for long-term growth, I would accept temporary fluctuations due to market influences.

Estate Planning

The purpose of estate planning is to:

Transfer your estate according to your wishes

Minimize estate taxes and expenses

Fund estate taxes

To avoid costly and prolonged probate, these documents need to be prepared in advance of one’s death:

Trust

Last Will and Testament

Power of Attorney

Health Care Directive

Charitable Remainder Trust

Tax planning

Project federal income taxes

Evaluate tax-minimizing strategies

Investigate tax-favored investments

With every financial decision and recommendation in a financial plan, tax planning needs to be strongly considered in all areas and at every phase.

At Executive Forums Silicon Valley, selected business owners and leaders work together to gain clarity, insight and accountability to ignite their leadership engines, grow their businesses and improve their lives. If you are interested in learning more about Business Owner Advisory Boards, Entrepreneurial Operating System (EOS), Stages of Growth, Value Builder System or becoming a member at Executive Forum Silicon Valley, please contact Glenn Perkins gperkins@executiveforums.com or call 408-901-0321. For more information visit http://www.execforumssv.com/.

Executive Forum Silicon Valley invited Emily Scott, a thought partner working with her clients to help unpack their money stories to improve their personal and professional financial decision-making, communications, and relationships. With no assets under management, Emily’s sole skin in the game is her clients’ peace of mind and clarity in discovering their money mindset, exploring their legacy, and determining their philanthropy. Emily works with financial advisors, and other professionals to help their clients understand the role of money in all aspects of their lives.

Identifying one’s own feelings about money

Ms. Scott started with a self assessment on a scale from 1- 10, to see the intensity of one’s feeling about one’s money, more or less categorized into four types of emotions:

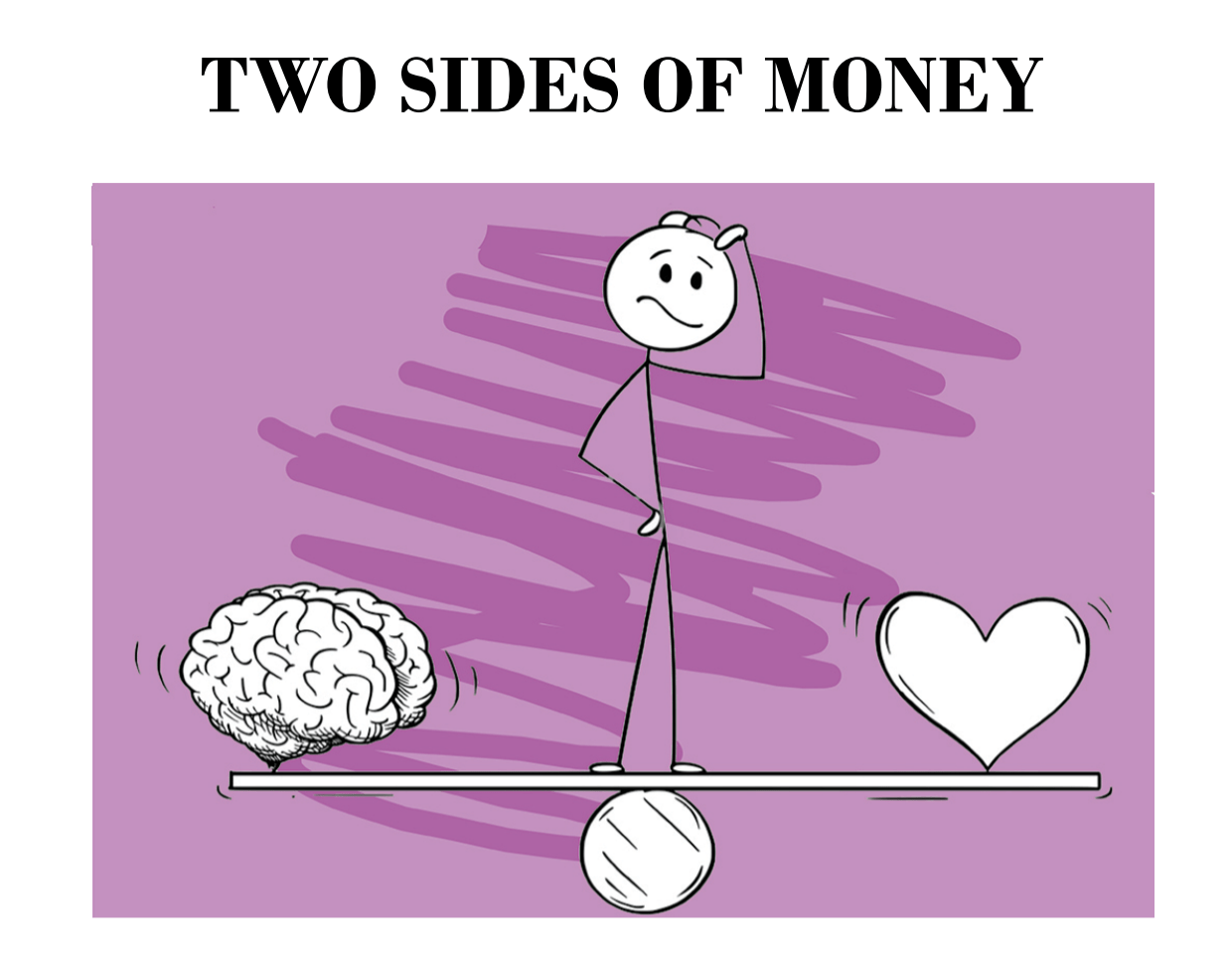

When it comes to decision making the personal side of money is more important than the technical side

There are two sides to money, the technical and personal sides. Both sides are equally important and complex, but it is the personal side that drives decision-making, said Emily.

The technical side includes aspects such as taxed, investments, estate planning, cash flow, risk management.

The personal side encompasses relationships, emotions, hopes and dreams, self-esteem, sense of well-being.

Aristotle said: “Knowing yourself is the beginning of all wisdom.”

Everyone’s relationship with money starts with one’s core beliefs about money. Our money story starts early in our lives by the implicit and explicit messages we receive on a daily basis. This story comes from our homes, our cultures, gender, media, and more. For most, we are taught to not talk about money and any feelings we have are deeply embedded and manifest in ways we don’t even realize.

The source of all money-related thoughts and behaviors derives from one’s core beliefs.

Thoughts and behaviors around money lead to outcomes and consequences.

Better outcomes with money depend on changing one’s beliefs, thoughts, behaviors

If you are not happy with your money situation, you need to start to adopt NEW beliefs, as shown in the below example of a “personal wealth mission statement”:

“I want my money to represent who I want to be as a human being, with my knowledge and emotions aligned to maintain my security, flexibility, freedom, and generosity.”

Several things need to happen in order to achieve better outcomes:

Recognize beliefs, thoughts, and behaviors that are detrimental to your new goals;

Rethink and reframe new beliefs and thoughts that are intended for better outcomes; Revisit these beliefs, to get clarity and confidence;

Align intentionality with developing new habits and routines for reaching your new goals;

Getting your subconscious (your “computer”) to work for you, until your goals are accomplished.

To get a personal consultation about changing your relationship with money, please contact Emily Scott’s email: emily@emilyscottand.com or call her at: (415) 609-1900.

At Executive Forums Silicon Valley, selected business owners and leaders work together to gain clarity, insight and accountability to ignite their leadership engines, grow their businesses and improve their lives. If you are interested in learning more about Business Owner Advisory Boards, Entrepreneurial Operating System (EOS), Stages of Growth, Value Builder System or becoming a member at Executive Forum Silicon Valley, please contact Glenn Perkins: gperkins@executiveforums.com or call 408-901-0321. For more information visit http://www.execforumssv.com/.

A Roadmap for Pivoting a Business Towards Future Growth

In times of turmoil, we hear the inevitable cry to pivot your business into a new set of products or services. Exactly how is that done? What are the steps?

Do we need a crisis to pivot our business?

Shouldn’t we always be looking to pivot our business?

And, if pivoting is so easy, why doesn’t everyone do it?

These questions were explored at the Executive Forums Silicon Valley Top Executive Forum this month through a presentation and discussion led by Beatrice Stonebanks (Stonebanks Sales Management Teams).

The discussion explored both the impact of the current COVID 19 environment as well as general long-term industry and buyer trends. After all, no one wanted to be like BlockBuster Video who missed the trend and technology of HOW consumers wanted to procure and engage, even though they knew all along about consumer demand for video content. Same goes with many taxi companies who did not innovate and pivot towards new ways of meeting customers’ needs for transportation and missed the trend and technology of HOW consumers wanted to procure and engage.

Ms. Stonebanks walked the members through some specifics on how to use industry reports to answer the following types of questions, as a roadmap to focus on:

What are the trends in your market?

Exactly why are your best customers buying from you?

What technology will be used to buy your products and services?

Where are the growth sectors that value similar characteristics?

What happens in your target markets if a Black Swan event happens?

How must you embrace technology to stay relevant to your customers?

This is a concise and straightforward method using just a few key questions to determine why your best customers value your product, service or company and what additional value you can provide.

The members were led through the “Stonebanks Sales Management 10 Step Process” that acts as a roadmap to help companies work through this process. A summary of the ten steps of this process are:

Access 2020 Tech Trends Report

Research Your Sector (or the sector you might pivot into)

Keyword Search a Term or a Specific Niche

Conduct an Ideal Client Summary

Create a Decision Matrix for Your Company

Choose your Preferred Target Niche(s)

Review the Top Ten Fastest Growing Sectors – Match with Your Niche

Analyze Optimistic and Pessimistic Trends in Selected Sectors

Adjust Your Products or Services Accordingly

Create Your Business Development Game Plan

Each specific member company was presented with a quick summary of the results of this process. For example, for one member who runs a full-service printing company, the following trends were identified. Although these types of trends are just the tip of the iceberg, consider how valuable this type of data-derived information can be in developing business growth plans. These trends were identified for the printing company:

print on packaging is a growth area – flexography, gravure

professional services to other printers

geographic collaboration (FTD model) are applicable

sector growing by 12% through 2024

This short article cannot do justice to the richness of the discussion around this process, and how it is relevant at all times, beyond COVID 19.

So pivoting is not that easy, however, there is a process that can be used. If you are looking to skate your company to where the puck will be (or how to use the puck in a completely new game), I recommend that you contact Beatrice Stonebanks (510 338-0896 www.stonebanks.net).

At Executive Forums Silicon Valley, selected business owners and leaders work together to gain clarity, insight and accountability to ignite their leadership engines, grow their businesses and improve their lives. If you are interested in learning more about Business Owner Advisory Boards, Entrepreneurial Operating System (EOS) or The Seven Stages of Growth, contact gperkins@executiveforums.com or call 408-901-0321. For more information visit http://www.execforumssv.com/.

Perhaps the best way to succeed in your business, is to work yourself out of your business.

The better your company runs on autopilot, the more valuable it will be when you’re ready to sell or transition.

A recent survey by The Value Builder Score found companies that would perform well without their owner for a period of three months are 50 percent more likely to get an offer to be acquired when compared to more owner-dependent businesses.

Let your vacation be a detective

There is no better justification for taking a blissful, uninterrupted holiday than to see how your company performs in your absence. To gauge your company’s ability to handle your absence, start by taking a vacation. Leave your computer at home and switch off your mobile. Upon your return, you’ll probably discover that your employees got resourceful and found answers to a lot of the questions they would have asked you if you had been in the building or on the end of an email or telephone call. That’s a good thing and a sign you should start planning an even longer vacation.

You’ll also likely come back to an inbox full of issues that need your personal attention. Instead of busily finding answers to each problem in a frenzied attempt to clean up your inbox, slow down and look at each issue through the lens of a possible problem with your people, systems or authorizations.

People – start with your people and answer the following questions:

Why did this issue or problem end up on my desk?

Who else is qualified to answer this question?

Why did the organization not contact and consult that person?

If nobody is qualified, who can be trained for the future?

In my many years of leading and working with companies, growing the capability of the team is the most important role of the leader.

Systems – next, look at your systems and procedures:

Could the issue have been dealt with if you had a system or a set of rules in place?

Whose department or area should be accountable for developing that system?

Can this issue be solved with system automation to remove the human element?

The best systems are hardwired and do not require human interpretation; but if you’re not able to lock down a technical fix, then at least give employees a set of rules to follow in the future.

Authorizations – You may be a bottleneck in your own company if you’re trying to control all the spending too much.

Did the employees know what to do but did not have any means of paying for the fix?

Can you put in customer service rules with financial limits of authority?

You might empower (and encourage) an employee to spend a specific amount with a specific supplier each month without coming to you first for authorizing every payment. Or you might give an employee an annual budget, an amount they can spend without seeking your approval.

Let your vacation strengthen your company

Given the fires that may need to be extinguished after the fact, taking a holiday may seem more of a hassle than it’s worth. But don’t be fooled – if you transform the aftermath of a vacation into systems and training that allow employees to act on their own, you’ll find the vacation is worth what you paid for it many times over. Your company will increase in value as it becomes less dependent on you personally.

At Executive Forums Silicon Valley, selected business owners and leaders work together to gain clarity, insight and accountability to ignite their leadership engines, grow their businesses and improve their lives. If you are interested in learning more about Business Owner Advisory Boards, Entrepreneurial Operating System (EOS), Stages of Growth, Value Builder System or becoming a member at Executive Forum Silicon Valley, please contact gperkins@executiveforums.com or call 408-901-0321. For more information visit http://www.execforumssv.com/.

Have you ever considered making it your primary goal to set up your business so that it can thrive and grow without you?

A business not dependent on its owner is the ultimate asset to own. It allows you to have complete control over your time so that you can choose the projects you get involved in and the vacations you take. When it comes to exit, a business independent of its owner is worth a lot more than an owner-dependent company.

Here are five ways to set up your business so that it can succeed without you.

1. Give Them A Stake In The Outcome

Jack Stack, the author of The Great Game of Business and A Stake In The Outcome wrote the book on creating an ownership culture inside your company: you are transparent about your financial results and you allow employees to participate in your financial success. This results in employees who act like owners when you’re not around.

2. Get Them To Walk In Your Shoes

If you’re not quite comfortable opening up the books to your employees, consider a simple management technique where you respond to every question your staff brings you with the same answer, “If you owned the company, what would you do?” By forcing your employees to walk in your shoes, you get them thinking about their question as you would and it builds the habit of starting to think like an owner. Pretty soon, employees are able to solve their own problems.

3. Vet Your Offerings

Identify the products and services which require your personal involvement in either making, delivering or selling them. Make a list of everything you sell and score each on a scale of 0 to 10 on how easy they are to teach an employee to handle. Assign a 10 to offerings that are easy to teach employees and give a lower score to anything that requires your personal attention. Commit to stopping to sell the lowest scoring product or service on your list. Repeat this exercise every quarter.

4. Create Automatic Customers

Are you the company’s best salesperson? If so, you’ll need to fire yourself as your company’s rainmaker in order to get it to run without you. One way to do this is to create a recurring revenue business model where customers buy from you automatically. Consider creating a service contract with your customers that offers to fulfill one of their ongoing needs on a regular basis.

5. Write An Instruction Manual For Your Business

Finally, make sure your company comes with instructions included. Write an employee manual or what MBA-types called Standard Operating Procedures (SOPs). These are a set of rules employees can follow for repetitive tasks in your company. This will ensure employees have a rulebook they can follow when you’re not around, and, when an employee leaves, you can quickly swap them out with a replacement to take on duties of the job.

You-proofing your business has enormous benefits. It will allow you to create a company and have a life. Your business will be free to scale up because it is no longer dependent on you, its bottleneck. Best of all, it will be worth a lot more to a buyer whenever you are ready to sell.

=============================================

At Executive Forums Silicon Valley, selected business owners and leaders work together to gain clarity, insight and accountability to ignite their leadership engines, grow their businesses and improve their lives. If you are interested in learning more about Business Owner Advisory Boards, Entrepreneurial Operating System (EOS), Stages of Growth, Value Builder System or becoming a member at Executive Forum Silicon Valley, please contact gperkins@executiveforums.com or call 408-901-0321. For more information visit http://www.execforumssv.com/ .

The Four Real World Employee Ratios that Can Drive Your Business

It’s a competitive jungle out there, and the most sought-after prizes aren’t treasure chests of money, but people. High performing employees to be specific. Regardless of employment levels, top companies know that success depends on not only attracting and retaining your most productive employees, but also on building a healthy set of employee performance metrics. This article will focus on four employee metrics that are not usually tracked, though they can make or break your business value. These key employee metrics are:

Employees per square foot

Customers per account manager

Ratio of Promoters to Detractors

Revenue per employee

If you’re planning to sell your company one day, tracking key ratios is a must. Acquirers like tracking ratios, and the more relevant ratios you can provide a potential buyer, the more comfortable they will become with the idea of buying your business. The bulk of the employee ratios that successful businesses need to monitor involve how human capital is most effectively used in a given enterprise.

Numerous sources can be found to confirm the following: “There is no doubt about the fact that the human asset is the key intangible asset for any organization. In today’s dynamic and continuously changing business world, it is the human assets and not the fixed or tangible assets that differentiate an organization from its competitors.”

There are four key employee metrics to keep your eye on, the first two having to do with efficiency and the last two focused on effectiveness.

Employees per square foot

By calculating the number of square feet of office space you rent and dividing it by the number of employees you have, you can judge how efficiently you have designed your space. Commercial real estate agents use a general rule of 175-250 square feet of usable space per employee. It’s not about crowding more employees into less space, it’s about workflow and productivity, so take virtual teams and work-from-home options into your calculations too.

Customers per Account Manager

How many customers do you ask your account managers to manage? Finding a balance can be tricky. Some bankers are forced to juggle more than 400 accounts, and therefore do not know each of their customers, whereas some high-end wealth managers may have just 50 clients to stay in contact with. It’s hard to say what the right ratio is because it is so highly dependent on your industry. Slowly increase your ratio of customers per account manager until you see the first signs of deterioration (slowing sales, drop in customer satisfaction). That’s when you know you have pushed it too far. You’re trying to create a balanced, high-performing team, where account managers can effectively spread their expertise over a full plate of customers, removing some of the waste in workflow management so that managers have their time well spent and customer needs are being met by an experienced resource.

Ratio of Promoters and Detractors

The Net Promoter Score® methodology, developed by Fred Reichheld and his colleagues at Bain & Company and Satmetrix, is based on asking customers a single question that is predictive of both repurchase and referral. It works by asking a single question, “On a scale of 0 to 10, how likely are you to recommend (insert your company name here) to a friend or colleague?” Now, as much as that can be an indicator of customer satisfaction, it can also be a telling question to ask of employees. The same principles apply, as employees are the single largest source of referrals for new hires, and referrals are a key indicator for longevity and productivity in your employees. Figure out what percentage of the employees surveyed give the company a 9 or 10, and label that your ratio of “promoters.” Calculate your ratio of detractors by figuring out the percentage of people surveyed who gave you a score of 0 to 6. Obviously the results need to be kept confidential if you’re doing the survey of employees, but the results are indicative of internal opportunities and work to be done. You calculate your Net Promoter Score (NPS) by subtracting your percentage of detractors from your percentage of promoters. The average company in the U.S. has a Net Promoter Score of between 10 and 15 percent while a good Net Promoter score is greater than 50 (Netflix, Amazon) and a world class Net Promoter Score is above 70 (Apple, Tesla, BMW). The glaring conclusion is that companies with an above-average Net Promoter Score grow faster than average-scoring businesses.

Revenue per Employee (RPE)

Payroll is the number one expense for most businesses, which explains why maximizing your revenue per employee can translate quickly to the bottom line. It’s a multi-faceted indicator of employee quality, company culture, employee-customer relations and the overall health of the business.

“Revenue per employee (RPE) is one of the most underrated metrics available for assessing business performance in a crowded marketplace.” Many leaders look at gross income and overall market share, but neither metric provides much actionable data. “If a competitor is achieving far higher RPE numbers than you, then you’ve got a pretty clear signpost towards areas for improvement.”

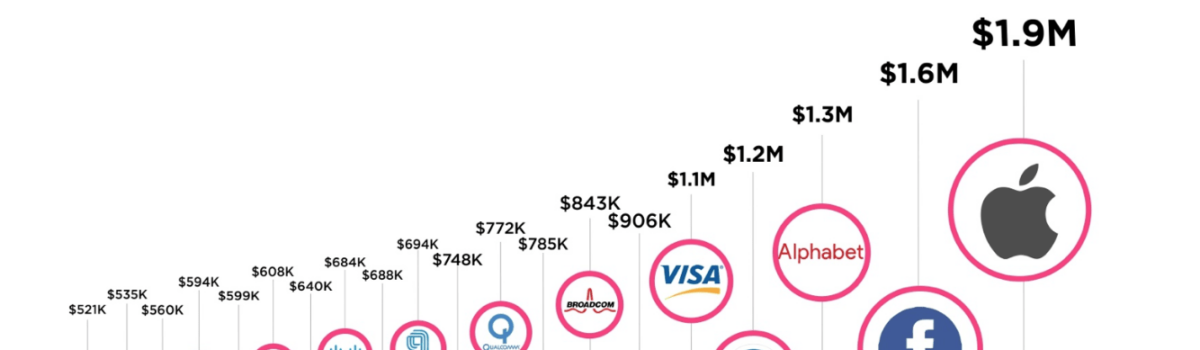

Amongst the largest corporations, average revenue per employee hovers at an astounding $1.3 million, with oil companies leading the way. Technology companies, where employee culture is considered some of the most innovative and efficient, put up some impressive RPE numbers as shown in the graphic above.

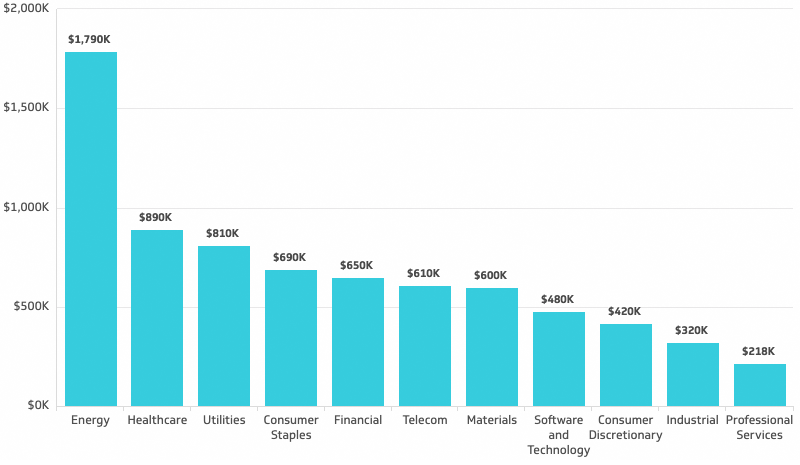

Some smaller companies struggle to cross the RPE threshold of $100,000, though their businesses are still wildly valuable (as size definitely does matter). Interestingly, smaller firms, which you would expect to be more productive than their larger competitors, actually average just over $100,000 per employee per year vs. almost $300,000 for the Fortune 500. All those systems and processes do count for something. Typical revenue per employee for various industries are shown below.

If you’re interested in benchmarking your industry, go to www.hoovers.com, the leading business database in the U.S. and search for larger companies in your industry. Click on the Fact Sheet that displays as an option and simply take revenues and divide by the number of employees.

Case Study – Revenue per Employee – The Container Store

An impressive case study can be made from the practices of The Container Store, the privately held retailer out of Texas, named one of the top places to work in the U.S. the past five years. They have a simple productivity formula: one great employee replaces three good employees; pay them twice as much ($20 per hour vs. the standard $10 a typical retailer pays) while having a lower total wage cost; and provide each employee with 160 hours of training. In essence, fewer higher paid smart people rather than a bunch of low paid “dump” folks! It’s your choice. And if you’re having a tough time recruiting employees, consider that The Container Store had 4000 people apply for the 40 positions they needed when they opened one of their retail stores in New York City. By building their business model from the very beginning to focus on garnering three times the productivity from sales associates, they can afford to pay them considerably above industry norm. The extensive training, in turn, helps to drive the productivity necessary to make the economics work. And the higher wages help to attract a better initial employee and retain the highly productive employees they create through their educational programs.

Now, it might seem logical to trim staff numbers to send your RPE ratios through the roof but don’t fall for it, as increasing workloads and lowering FTEs has been proven to negatively impact productivity in the long term.

The think tank at McKinsey has looked at RPE and at the intangible value that human capital contributes to businesses, and their results are thought-provoking:

“The vast majority of companies still gauge their performance using systems that measure internal financial results—systems based on metrics that don’t take sufficient notice of the real engines of wealth creation today: the knowledge, relationships, reputations, and other intangibles created by talented people and represented by investments in such activities as R&D, marketing, and training.

Companies fill their annual reports with information about how they use capital but fail to reflect sufficiently on their use of the “thinking-intensive” people who increasingly drive wealth creation in today’s digital economy.”

They go so far as to suggest a remedy for company CEOs and leadership that might be stuck in the past. “To boost the potential for wealth creation, strategically minded executives must embrace a radical idea: changing financial-performance metrics to focus on returns on talent rather than returns on capital alone. This shift in perspective would have far-reaching implications—for measuring performance, for evaluating executives, even for the way analysts measure corporate value. Only if executives begin to look at performance in this new way will they change internal measurements of performance and thus motivate managers to make better economic decisions, particularly about spending on intangibles.”

When it comes to building or presenting the value of your business, whether you’re looking to sell it or not, the data picture that you present truly does speak volumes. Like an artist using multiple textures and colors, data ratios, especially as they relate to employee efficiency metrics, can tell a much more compelling story than just looking at gross revenues or inventory turns.

If you’re still wondering if revenue per employee translates into bottom line performance, consider this: one recent study in the technology industry (software, hardware, IT services, etc.) found that the top 10% of companies ranked by performance had roughly twice the revenues per employee as the average. Now, can you afford not to examine RPE in your own business? Something to think about, hard.

At Executive Forums Silicon Valley, selected business owners and leaders work together to gain clarity, insight and accountability to ignite their leadership engines, grow their businesses and improve their lives. If you are interested in learning more about Business Owner Advisory Boards, Entrepreneurial Operating System (EOS), Stages of Growth, Value Builder System or becoming a member at Executive Forum Silicon Valley, please contact gperkins@executiveforums.com or call 408-901-0321. For more information visit http://www.execforumssv.com/ .